- 2 replies

- 4,890 views

- Add Reply

- 4 replies

- 4,213 views

- Add Reply

- 6 replies

- 3,614 views

- Add Reply

- 3 replies

- 1,804 views

- Add Reply

- 4 replies

- 999 views

- Add Reply

- 9 replies

- 5,263 views

- Add Reply

- 2 replies

- 1,309 views

- Add Reply

- 6 replies

- 1,659 views

- Add Reply

- 0 replies

- 708 views

- Add Reply

- 2 replies

- 1,611 views

- Add Reply

- 4 replies

- 1,629 views

- Add Reply

- 5 replies

- 4,189 views

- Add Reply

- 4 replies

- 12,536 views

- Add Reply

- Sole-Prop, owner-only client comes in with a 401(k) Plan with a value of $70,000 as of 12/31/2023

- They also have a pre-existing SEP valued at $190,000 as of 12/31/2023. Went "dormant," and 401(k) was adopted in a later year.

- 5500-EZ was not filed for 2023

- 6 replies

- 2,887 views

- Add Reply

- 5 replies

- 2,387 views

- Add Reply

- 1 reply

- 886 views

- Add Reply

- 3 replies

- 2,984 views

- Add Reply

- 3 replies

- 1,678 views

- Add Reply

- 10 replies

- 2,506 views

- Add Reply

- 4 replies

- 2,892 views

- Add Reply

Mandatory Auto Enrollment Effective Date

Admittedly, the more I read about the MAE and when a small business crosses over the 10 employee threshold, the confused I become. If a plan was adopted and effective 1/1/2023, but hires the 11th employee on 4/1/2025, is the effective date when the plan has to add MAE 1/1/2027?

Do I have to continue filing 5500-EZ?

Hi

2019 5500-EZ was filed with less than 250k in assets -first year of the plan/filing but stopped filing in subsequent years and assets are still under 250k.

Was there a continuation requirement because initially it was filed?

Thanks

Partial Plan Term--Do Accounts HAVE to be distributed?

Before this plan came to us, there was a partial plan termination.

Many of the accounts were distributed, but not all. Those that remained just were given accelerated vesting.

Do the accounts of participants involved in a partial plan term HAVE to be distributed? Or can they stay in the plan?

Question about (QRP) Qualified Replacement Plan investments from terminated DB plan

We’re dealing with excess assets from a terminated traditional defined benefit (DB) plan that are being moved into a 401(k) profit sharing plan as part of a Qualified Replacement Plan (QRP).

Can the QRP funds be moved into a cash or money market account earning little or no interest while the rest of the plan's assets remain invested? This is a one-participant plan, not sure if that makes a difference.

The existing plan assets are invested in volatile securities, and the account owner is concerned that market swings in the suspense account could prevent us from using up all of the QRP funds within the required 7-year period. I couldn’t find anything indicating that QRP funds must be invested in the same way as the rest of the plan — does anyone know if that's a requirement?

Appreciate any insights!

Advisory letter used for (ostensibly) pre-approved plan, ostensibly dated 9/30/2014

Is this even possible? I didn't think the IRS did any Advisory letters for "pre-approved" plans that early. Have NOT seen the actual document or IRS letter to confirm what the audit firm is saying...

What are the difficulties of a brokerage window?

For an individual-account retirement plan with participant-directed investment that gets Ascensus’ recordkeeping services, the plan’s sponsor (which also is the plan’s administrator and trustee) is considering adding a Schwab Personal Choice brokerage window, restricted to mutual-funds-only.

Unlike other employee populations in which only a relatively few participants use a brokerage window, almost all participants would use the mutual-funds window.

The employer pays Ascensus’ fees for all still-employed participants, and likewise would pay Ascensus’ incremental fees for pulling the brokerage accounts into the recordkeeping.

The counts of participants, all of whom have a plan account balance, are such that the plan every year will require an independent qualified public accountant’s audit of the plan’s financial statements. An Ascensus-aligned trust company is the plan trustee’s custodian.

The plan does not use Ascensus or a TPA to test coverage, nondiscrimination, or top-heavy measures.

BenefitsLink neighbors, what difficulties should I advise this plan sponsor to consider in its decision-making about whether to add the brokerage window?

LLC 401K Contribution(s)

We have a two member LLC husband, wife. She does not share in the profits. We keep getting different answers on what they can as members contribute to the company 401K. Best I can come up with is the wife would be limited to her guaranteed payments and her elective deferral and the husband would have his elective deferrals and limited by his compensation which is should be the profit. So for him it would be up to 76500. Any assistance with this would be appreciated. Thanks!

How can other professionals help an actuary?

Actuaries, for situations in which you must integrate or at least align your work with others’ work—or doing your work depends on information from another professional’s work—what can other professionals do to help, or at least not interfere with, your work?

My law school courses for LLM and MST students include lessons on how professionals of all stripes should be respectful of another’s profession, and should do one’s own work in ways that support another professional’s work. I hope to fill out an explanation of how lawyers, accountants, and other professionals can work in ways that help an actuary do her work.

This can be about an actuary’s work for health, disability, and other welfare benefit plans; pension and other retirement plans; or pricing any kind of insurance.

What could someone else do to make your work as an actuary a little easier?

And for a BenefitsLink neighbor who is not an actuary, what work steps improve your working relationship with an actuary?

QACA Match - formula not being capped

I have a prospective client who asked me to review their plan. The QACA match formula is 200% up to 5% of pay. Current TPA (bundled provider) is not capping. Everyone is getting 200% of deferrals. One person is receiving a 10% match. How would you fix this since the match exceeds 6%? And they aren't complying with the plan doc?

Frozen prior to September 2005 no aftap restrictions

Hi,

As per 1.436-1(d)(4) a plan that was frozen plan prior to 9/1/2005 is not subject to the AFTAP Restrictions including that it can pay lump sums. If the AFTAP calculations are above 100%, however, there were no actual AFTAP certifications done, is there any basis for the SB to show the AFTAP as being above 100% and it will be based on the signing of the SB (since there are no AFTAP restrictions) or must the SB show the AFTAP as 60% ?

As why file with 60% and possibly draw attention of the electronic system, if there are really no AFTAP restrictions for this plan anyway?

Thank you

Hardship Determination

I have a client that has not yet adopted the self-certification for Hardship Distributions. I have a situation where it doesn't distinctly fall under a Hardship per the IRS Safe Harbors, but it's obvious there is a financial need.

The participant needs to move to a new rental with their parents, who are terminally ill.

So it's not the purchase of a primary residence and it's not for the medical bills, but they are moving/renting in order to get treatment and care for them.

Is this a situation where we can still approve the Hardship?

New Plan to me -> Business has Fiscal Year, Plan has Calendar Year

I have never run into this situation where the business has a June FYE and the plan has a calendar PYE. Is this common? Allowed? A nightmare to administer?

Thoughts? recommendations?

Thanks

ACA Requirements when employee moves from full time to part time

We have an employee who has moved from a full-time position to a part-time position mid year. Under the ACA, do we have to keep this employee on our benefits for the remainder of the stability period? Or, can we terminate benefits because the employee is no longer in an eligible class?

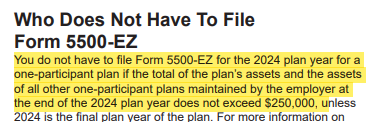

Pre-Existing SEP - First year 5500-EZ Filing for 401(k) Plan

If the SEP was established as a formal plan for the business at some prior date and was never formally terminated but simply went dormant, should the value be included in the asset total for determining the $250,000 threshold? 5500-EZ Instructions say the threshold determination includes "all other one-participant plans maintained by the employer."

I realize we treat a SEP as no longer being "maintained" when it is no longer receiving contributions, but I'm concerned about the implications in a 5500-EZ situation . . . not that anybody would know there was a SEP because there has never been a formal filing, BUT . . . I am curious!

We are taking over for the 2024 plan year. The concern is, should we also have the client file a 2023 Form 5500-EZ for the 401(k) under the Penalty Relief Program . . . ?

Amending QDRO

ERISA Preemption of State Legislation Prohibiting Investments tied to Chinese/Foreign Adversaries

Looking to find any case law that concerns ERISA preemption of state legislation limiting the investment scope of pension plans concerning investments tied to China (or similar foreign adversaries).

Note that last month 17 AGs gave notice to Blackrock, and similar providers, that inadequate disclosures (of material risks) for funds with Chinese investments potentially constituted a breach of fiduciary duty.

https://www.asppa-net.org/news/2025/2/chinese-investments-evoke-concern-of-state-ags/

Similar federal legislation is also in the works:

https://www.congress.gov/bill/118th-congress/house-bill/4008

CG, right?

Company A, Father owns 50%, Son own 50%. Company also employs son's mother and son's wife. Company B is 100% owns by mother, mother and father are not married. This is a B/S CG, right?

I file or other methods

Hi,

Thank you, as always, for the all your insights and informative responses. Our Pension reporting system (filing 5500 etc) is having technical issues. Until we resolve the issues:

1 . Are there alternate methods that we can use to file a few 5500s.

2. Does I file work similar to as when we file as third party signs and files for the client from our regular reporting program?

3.And is it easy to resgister and get started to use i file?

4. Are there any other alternatives that we can use to get these 3 or 4 5500 filed?

Thank you very much.

Safe Harbor Plan and Sale/acquisition

Looking for some thoughts on this situation. Buyer company A is seeking to buy target company B. Company B is owned by a larger company and there are more than 2 401k plans in this controlled group. Buyer company A sponsors a safe harbor plan and Target company B sponsors a safe harbor plan. Buyer A does not want to take over this plan they want it terminated before the sale, and then have participants roll over their balance to company plan A. Are there any options to terminate Company B safe harbor plan? The problem I see is that Seller B is part of a controlled group, and the successor alternative plan comes into play - if seller B terminates the plan, the termination is not a distributable event since there is another 401k in that controlled group. If they do not terminate the plan before the sale, and Buyer A takes over the plan, the successor 401k plan rule still comes into plan and if Buyer A terminates the plan it is not a distributable event. I see no clear guidance where you can merge a terminated safe harbor mid-year into another safe harbor plan (maybe this is ok?), or that you can distribute assets in a terminated safe harbor plan if there is a successor plan. Any thoughts?

Employee misled re: marital status on health enrollment forms

Here in California, just discovered yesterday that an employee has been misrepresenting that his domestic partner was his spouse on his health insurance enrollment forms for the last four years. Found out because he just told me he was about to get married later this month! I don't believe it was malicious, he's just really clueless about this stuff.

Anyway, I don't believe she is a registered domestic partner (that would be uncharacteristic of him, although I could be wrong). Her premiums have been paid pre-tax through payroll deferrals and she also used his HRA last plan year. Regardless of whether or not she is registered, I know that the IRS does not generally allow pre-tax premium deferrals and HRA participation for domestic partners.

Any advice on what to do now? Go back and try to make four years of corrections or just move forward since they are about to get married in 3 weeks?

And yes, going forward, we'll ask for marital status verification...

Thanks in advance!

Featured Jobs

July Business Services (JULY)

(Remote)")

Senior Retirement Plan Analyst - DC Plans

M2B Retirement Consulting LLC

(Remote / PA)

ESOP/KSOP Processing Specialist

BPAS

(Utica NY)

Retirement - Client Services Manager

Navia Benefits

(Remote)

July Business Services

(Remote)Participant Services Representative

BPAS

(Spokane WA / Hybrid)Loren D. Stark Company

(Remote / NJ / NV / TX)

Transaction Coordinator II (Brokerage accts)

MAP Retirement

(Remote)

MAP Retirement

(Remote)